A Guide From Your Mortgage Broker & Realtor Team

If you are renting right now and thinking about owning a home one day, the path forward may be easier than you think! As a mortgage professional working alongside a local real estate expert, this is how we help renters understand the process without getting overwhelmed so they can be ready with confidence.

Common Myths That Stop Renters From Buying

When most renters think about buying a home, a few common ideas come to mind right away. These ideas sound true, but they often are not.

Myth 1: You Need 20% Down

This is one of the most common beliefs renters have.

Many people think they must save 20% of the home price before buying. That idea alone stops a lot of renters from even looking into homeownership.

In reality, many buyers put much less down. There are programs, including government backed options, that allow down payments as low as 3.5% or even 0%.

The right amount depends on the loan and the buyer. There is no single number that fits everyone.

Myth 2: You Need Perfect Credit

Many renters believe their credit score has to be near perfect before they can even think about buying a home.

In reality, approval is often possible with credit scores in the 500s, depending on the loan program and overall financial picture.

Small issues, past mistakes, or limited credit history do not automatically stop someone from buying. In many cases, small changes can make a big difference. Many buyers are surprised to learn they are closer than they thought. Sometimes it is not about being perfect. It is about understanding your options and creating a plan.

Myth 3: Your Job Has to Be 100% Stable

Another common myth is that you must be in the exact same job for two full years before qualifying for a mortgage.

The truth is lenders are typically looking for a two-year history in the same line of work — not necessarily the same employer.

Promotions, raises, and even job changes can still work in your favor, especially if they show growth within your field. Self-employed borrowers are also reviewed based on a two-year history of income, not perfection or zero changes.

Career growth does not automatically disqualify you. In many cases, it can actually strengthen your file.

The key is reviewing your specific situation and understanding how your income will be calculated.

Myth 4: It’s Better to Wait for the Perfect Time

Many renters think they should wait for interest rates to drop, home prices to fall, or a more convenient moment in life before buying a home.

In reality, there is no universal “perfect time.” What may be right for one person could be wrong for another. Timing should be based on your personal financial situation, goals, and readiness—not headlines or market predictions.

Waiting for a hypothetical ideal moment can mean paying higher rent or missing opportunities. Prices might rise while rates drop, or vice versa; there is no way to predict the future with certainty.

The best time to buy is when it makes sense for you. Being prepared and understanding your options allows you to make a confident, informed decision.

Myth #5 The Home Has to Be in Perfect Condition

Many renters assume that a home must be completely move-in ready or flawless to qualify for a mortgage.

In reality, homes only need to meet basic safety and livability standards. Cosmetic issues like outdated kitchens, older flooring, or paint colors typically are not deal breakers.

There are also renovation loan programs, such as FHA 203(k) and Fannie Mae Homestyle loans, that allow buyers to finance certain repairs or improvements into the mortgage. This means that homes with potential—rather than perfection—can still be excellent opportunities.

Understanding what is truly required versus what is cosmetic can open doors to more options and help buyers see the potential in a home.

Myth #6 It’s Always Best to Go to Your Bank or Credit Union

Many renters believe that the bank or credit union where they already have an account is automatically the best place to get a home loan.

While banks and credit unions can be solid options, they typically offer only their own in-house loan products. A mortgage broker can shop multiple lenders and programs to find the loan structure that best fits a buyer’s specific situation.

Having flexibility and access to multiple options can make a meaningful difference in approval, loan terms, and overall satisfaction. The goal isn’t just getting a loan—it’s getting the right loan for your situation.

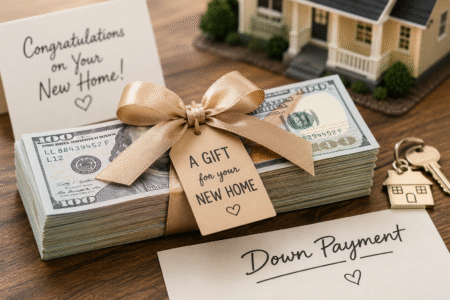

Myth #7 You can’t use gifted money towards the purchase of a home

Many renters believe that you can’t use gift money to buy a house, but in most cases, you absolutely can.

Many loan programs allow gift funds from family to cover part or even all of the down payment.

If family wants to help, that can be the difference between renting and owning.

There are some guidelines and documentation required. They can’t just Venmo you $10k. But I’m here to guide you through it to make it easy!

Why These Myths Matter

These myths keep renters on the sidelines.

Once you replace them with real information, buying starts to feel less scary and more possible.

And that is what we are here to do for you!